InsightsSovereign rating review Q3 2021: Getting ready to rise again?

Sovereign rating review Q3 2021: Getting ready to rise again?

Following the H1 lull, the Big Three agencies’ sovereign rating actions have picked up but remain slow relative to historic norms.

Dr. Moritz Kraemer Oct 11, 2021

Following the H1 lull, the Big Three agencies’ sovereign rating actions have picked up but remain slow relative to historic norms.

The numbers of upgrades and downgrades were balanced for the first time since the outbreak of the pandemic, while the ratings outlook continues to improve.

At CountryRisk.io, our assessments of sovereign risks also became more balanced: our credit scores deteriorated for 16 sovereigns but improved for 15.

Signs of life

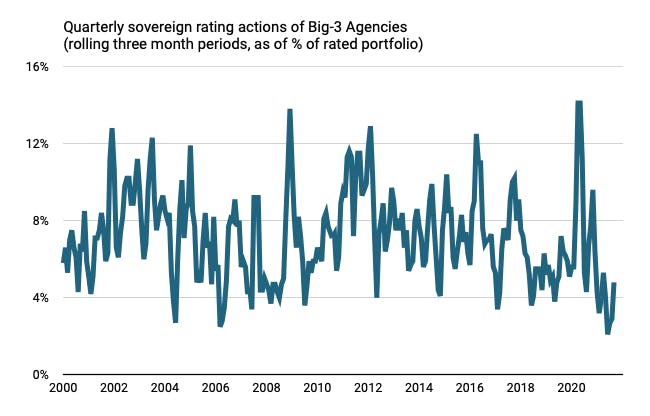

When it comes to sovereign rating actions by the Big Three global rating agencies (Fitch, Moody’s and S&P Global), the second quarter of 2021 was the most inactive on record (1). June saw no sovereign rating action at all, something that last occurred in 1993 just after Bill Clinton moved into the White House. With the first half of 2020 having seen a torrent of pandemic-induced rating changes (see Figure 1), 2021 has so far been the calm after the storm.

The Big Three started to show signs of life in Q3, although the share of rated portfolios that saw rating changes remains well below the norm. We expect a further mild pick-up of activity during Q4—typically a busy season for sovereign rating analysts (2).

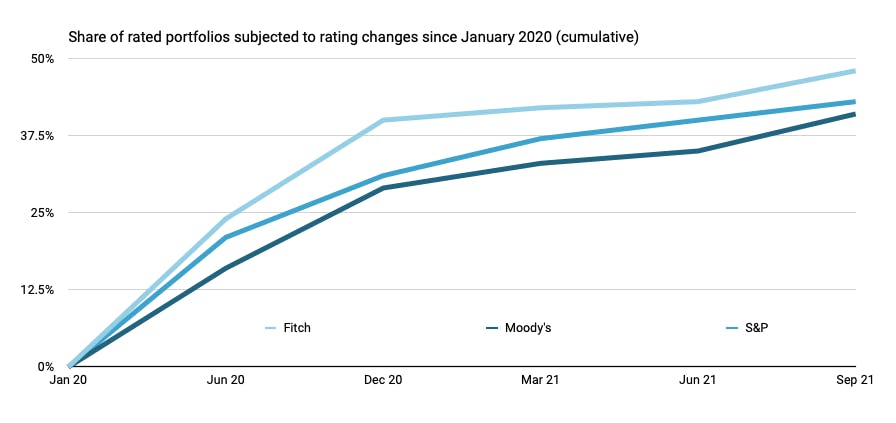

Moody’s continues to play catch-up. Fitch was the fastest out of the rating adjustment blocks in the early days of the pandemic, changing 21% of its sovereign ratings between March and May 2020—almost all downwards. During the same period, Moody’s changed just 8% of its ratings. As illustrated in Figure 2, Moody’s and S&P have been catching up throughout 2021.

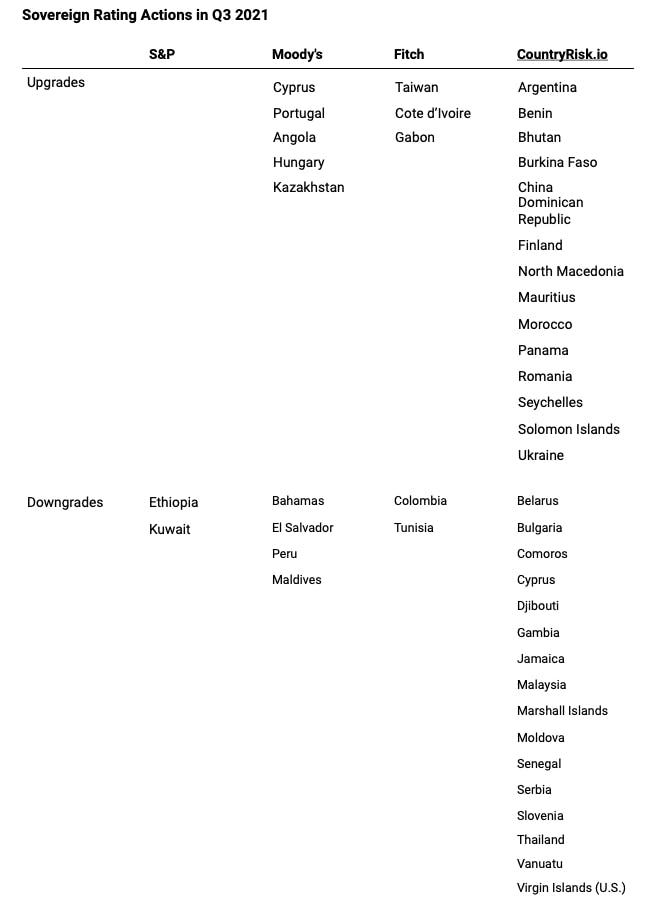

Upgrades and downgrades are back in balance. Figure 3 shows that there were identical numbers of upgrades and downgrades in Q3, breaking the negative balance of rating changes for the first time since the pandemic began. And with the balance of rating outlooks also improving (see below), we now think that Q4 could finally bring a (slightly) positive balance of rating changes. In short: the worst may be behind us.

Africa’s tentative comeback

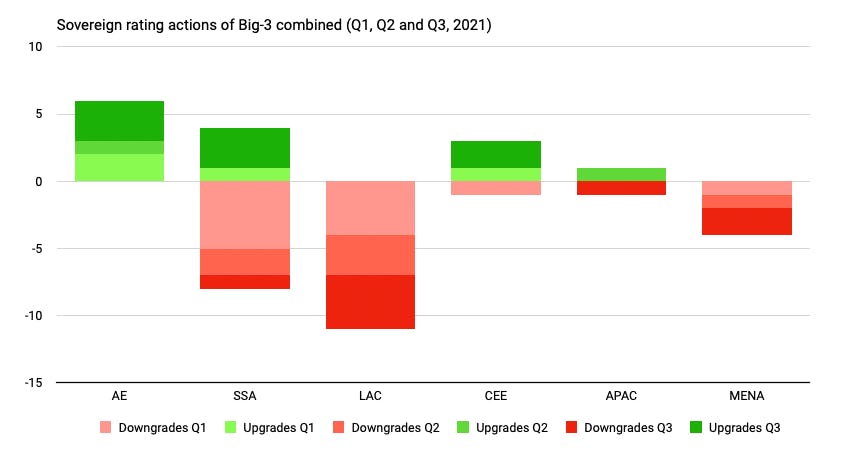

Latin American downgrades keep coming. In terms of regional rating actions, it was another dreadful period for Latin America and the Caribbean (LAC). In Q3, LAC clocked up another four downgrades, accounting for half of all downgrades globally (for a list of all rating actions, see Table 1) and continuing an equally terrible year for the region in which it has suffered 11 downgrades and zero upgrades (Figure 4). The only other region without any upgrades in 2021 is the Middle East and North Africa, which also had a bad third quarter with rating cuts for Kuwait (S&P) and Tunisia (Fitch).

Africa rising. The Q3 ratings news was brighter in Sub-Saharan Africa (SSA), where upgrades outnumbered downgrades by three to one. This may be because the wave of defaults that the Big Three agencies feared has not come to pass—or, at least, it hasn’t yet. As we have pointed out previously, we believe that much of SSA remains at risk of sovereign debt crises. A coherent and lasting solution to African over-indebtedness remains elusive, and we aren’t holding our breaths for a breakthrough at the upcoming IMF Annual Meeting. SSA is also the only region with rating actions in both directions during Q3, with upgrades to the ratings of Cote d’Ivoire, Gabon (by Fitch) and Angola (by Moody’s) standing against the sole downgrade of Ethiopia (by S&P).

Wealth attracts many friends

Once again, only the advanced economies can be said to have had an unambiguously positive quarter, with another three upgrades (Portugal and Cyprus by Moody’s, and Taiwan by Fitch) extending a clean sheet that we expect to remain downgrade-free for the rest of the year. This continues a trend that began in 2020, when agencies let rich countries off the downgrade hook despite the material deterioration of their fundamentals.

S&P has done the most to accommodate rich countries, which last downgraded an advanced economy over half a decade ago when it reduced the UK’s rating in the aftermath of the Brexit referendum (3). In the years since, rich countries’ ratings at S&P have only gone up—never mind that their public debt ratio has surged from an already-high 105% of GDP in 2016 to 123% this year (4).

We beg to differ with a more sober view on rich economies

At CountryRisk.io, we continue to believe that this lenient treatment of advanced economies may be due to a pro-rich bias. In our view rich countries remain subject to deteriorating credit risk. Our easy-to-use platform generates sovereign risk scores algorithmically—beyond selecting the input variables and sources, we apply no further discretion. Although we convert our sovereign risk scores into the standard rating scale symbols for comparability, our scores are not ‘ratings’ in the regulatory sense. CountryRisk.io does not hold a rating license and has no intention of applying for one. Nevertheless, we designed our platform’s sovereign risk scores to measure the same credit risks as the equivalent regulatory-approved ratings from the Big Three agencies.

Our credit scores show a continued weakness in advanced economies (Figure 5 and Table 1). We also take a dimmer view of Central and Eastern Europe (CEE), where the Big Three made more upgrades than downgrades this year. On aggregate, our risk scores are still slightly skewed down (16 downgrades versus 15 upgrades) as the social, economic, and financial consequences of the pandemic continue to make themselves felt. We explained this conclusion in greater detail in our risk update following the IMF and World Bank Spring Meetings.

Sparing highly rated sovereigns from downgrades also makes little statistical sense. Historic default data suggests that the probability of default changes only incrementally between ratings at the top of the scale. In contrast, reducing an already-low rating by the same number of notches indicates a more significant increase in the likelihood of default (5). Therefore, a constant increase in default probability should lead to bigger downgrades at the top of the ratings ladder, where most rich countries reside. And, unlike the Big Three’s rating actions, this is what our sovereign risk scores have shown since COVID-19 entered centre-stage.

A closer look at individual rating actions

Moody’s upgraded Portugal to BBB (or Baa2 in Moody’s-speak), driven largely by “Moody's confidence that Portugal's debt burden will decline in the coming years.”

We’ve seen this movie before. In August 2019, Moody’s improved the outlook on Portugal’s ‘BBB-’ rating to positive because, as they said at the time, “The continued improvement in Portugal’s fiscal performance [is] now expected to improve the country’s key debt metrics at a faster pace than anticipated a year ago.” In fact, Portugal’s debt has since increased rapidly, from 117% of GDP to over 131%—which is not an improvement, let alone one that was “faster than anticipated”. In fairness, the Portuguese authorities managed the economy’s emergence from the deep euro slump admirably, and even eked out a small fiscal surplus in 2019. But that’s not the point. The point is that, despite the refutation of their outlook by what actually happened, Moody’s upgraded Portugal anyway. This is the kind of thing that makes it increasingly difficult to take rating agencies’ “forward guidance” literally, or even seriously.

Rating actions like that on Portugal raise an interesting question: are ratings becoming more relative? More specifically: will downward rating pressure mount for all if fundamental credit metrics deteriorate for all? Or will the Big Three apply the judgmental component of their methodologies to treat sovereigns whose metrics exhibit (relatively) smaller deterioration as equivalent to an improvement meriting positive action? If so, this would be a clandestine break with the decades-long practice in which agencies adhered, without fear or favour, to their quantitative thresholds. Although a ‘better-than-feared’ (or ‘better-than-peers’) argument could perhaps be deployed against the charge that deteriorating fundamentals should have led to a downgrade, the notion that such an argument could justify an upgrade is a stretch to say the least. We have documented before how the Big Three agencies have moved their goalposts in the recent past, and the anecdotal evidence suggests that the agencies’ methodological forbearance is directed predominantly towards advanced economies as well as CEE countries. As it happens, these states are also home to the regulatory authorities that could cause the Big Three some serious trouble.

Cyprus was another noteworthy upgrade (to BB+) by Moody’s, bringing it within touching distance of investment grade. It is also another example of a ‘could’ve-been-worse’ upgrade. In September 2019, Moody’s gave Cyprus a positive outlook, ostensibly because its “bank-related exposure to event risk continues to decline” and its government debt ratio was expected to fall to “around 75%” by 2023. It also said, “[Cyprus’s] credit profile [a.k.a. rating] could weaken” should fiscal or economic deterioration “cause a reversal of the supportive fundamental debt trend.” So, where are we today? According to Moody’s, Cyprus’s debt stood at 119% last year. In July, Moody’s upgraded the country’s rating anyway, in part due to a “reduction in Cyprus's exposure to event risks because of a decrease in banking sector risks”—which is pretty much the same reason it gave for the positive outlook two years earlier. A little double-counting goes a long way.

Colombia was downgraded to non-investment grade (BB+) by Fitch on 1st July, with S&P having already done so in May. Following its negative outlook for Colombia issued in December, we can expect Moody’s to follow soon. Recent academic research showed that agencies tend to stick to their pre-defined regulatory review rhythm come hell or high water—so, since Colombia has been subject to an annual review last December, we should expect the Moody’s downgrade this upcoming December. This is another example of the observed pattern in which S&P leads with a downgrade across the investment grade divide, with the other agencies following suit once S&P had broken the ice. That said, Colombia could also be an example of a herd mentality, with each agency eying up the others’ decisions: once one agency moves, the others join in the same direction.[1] In contrast, our risk scores and derived ratings are purely quantitative, which immunises them from cross-referencing and ratings contagion.

Kuwait received its second S&P downgrade in a year in July (this time to A+, with a negative outlook maintained) after having kept it stable for almost a decade. Not coincidentally, this occurred 364 days after the first downgrade—another example of the agencies’ habit of reviewing a sovereign’s rating by committee when it is ‘due’ for regulatory purposes, instead of when things actually change on the ground (see comment on Colombia above). S&P’s rationale for its latest downgrade is interesting: “Due to parliamentary opposition, the government has so far been unable to pass a law giving it the authority to issue debt or gain immediate access to its large stock of accumulated assets.”

Peru saw Moody’s cut its rating (to BBB+) in September, the first time in two decades the sovereign has had to endure a downgrade. The agency argued that Lima suffers from a “continuously polarized and fractured political environment,” which it says has increased political risk and “materially weakened policymaking capacity”.

If the lack of authorisation for government borrowing (Kuwait) and a polarised political environment (Peru) can lead to downgrades, should President Biden’s ears be burning? Probably not. As we described earlier, the US is unlikely to be held to the same taxing standard as emerging sovereigns.

The sovereign weathervane: ratings outlooks turning more positive again

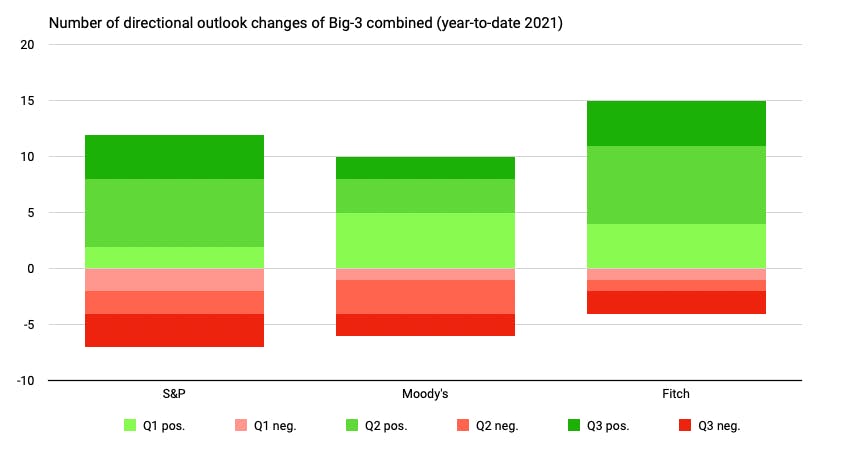

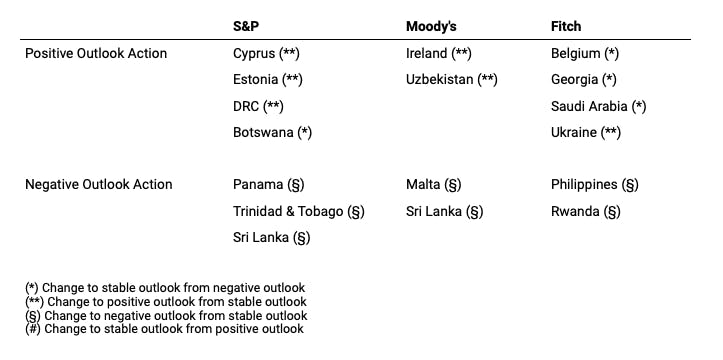

At all agencies, the outlooks keep improving. Unlike CountryRisk.io, the Big Three use rating outlooks to indicate whether the next change for a sovereign is more likely to be an upgrade (in the case of positive outlooks) or a downgrade (negative outlooks). So far this year, every agency has shown a strong tendency to improve outlooks (see Figure 6 and Table 2 for details) (6). This may indicate that, as far as the agencies are concerned, the worst is likely behind us in terms of net downgrades.

The pattern we saw in rating changes is mirrored in the Big Three’s rating outlooks. Advanced economies and CEE sovereigns once again saw their outlooks brighten most (see Table 2). Although advanced economies make up only 29% of all sovereigns rated by the Big Three, they accounted for 40% of positive outlook changes and only 14% of negative ones in Q3 (only tiny Malta received a negative outlook from Moody’s) (7). This suggests that we can expect the directional ratings divide between rich and poor countries to continue through the rest of this year and well into 2022.

Note: The sovereign coverage on September 2021 is as follows: Fitch 116, S&P 125, Moody’s 135 and CountryRisk.io 190. For each agency all ratings included on tradingeconomics.com are considered, which excludes some jurisdictions that are less than fully sovereign (e.g. emirates or UK overseas territories).

[1] All sovereign ratings data are taken from tradingeconomics.com.

[2] Between 1991 and 2020, a higher proportion of rating actions were taken in Q4 (27.3%) than in any other quarter of the year.

[3] S&P Global ratings: Sovereign Ratings History, monthly (subscriber access only). S&P downgraded Hong Kong in 2017, but that was due to the fact that China (not an advanced economy according to the IMF classification) was itself downgraded—for obvious reasons, Hong Kong’s rating is tied to (but higher than) China’s.

[4] IMF World Economic Outlook Database, April 2021.

[6] We exclude outlook changes that coincide with a rating change in the indicated direction of the previous outlook. For example, if a sovereign is upgraded as its outlook is changed from positive to stable, that outlook change would be excluded from the count.

[7] The respective percentages for advanced economies’ shares in Q2 were 27% of all positive outlook changes and 0% of negative outlook changes. See Table 2 in the Q2 ratings review.