African sovereign debtors aren't over the hump yet

African sovereign bonds have been rallying this year. But traditional credit metrics show very high vulnerability to debt distress. Our own credit assessments provide indications that risks may be rising in many countries.

Dr. Moritz Kraemer

Jun 08, 2021

African sovereign bonds have been rallying this year. But traditional credit metrics show very high vulnerability to debt distress. Our own credit assessments provide indications that risks may be rising in many countries.

In African debt markets, happy days are here again

Despite poor progress on vaccinations and the International Monetary Fund’s (IMF) warning about “divergent recoveries”, investors in African sovereign debt have regained the spring in their steps in recent weeks. This renewed buoyancy comes on the back of a robust recovery of commodity prices and the prospect that the expected increase in special drawing rights (SDR) issuance by the IMF will throw poorer countries a lifeline, potentially bailing investors out.

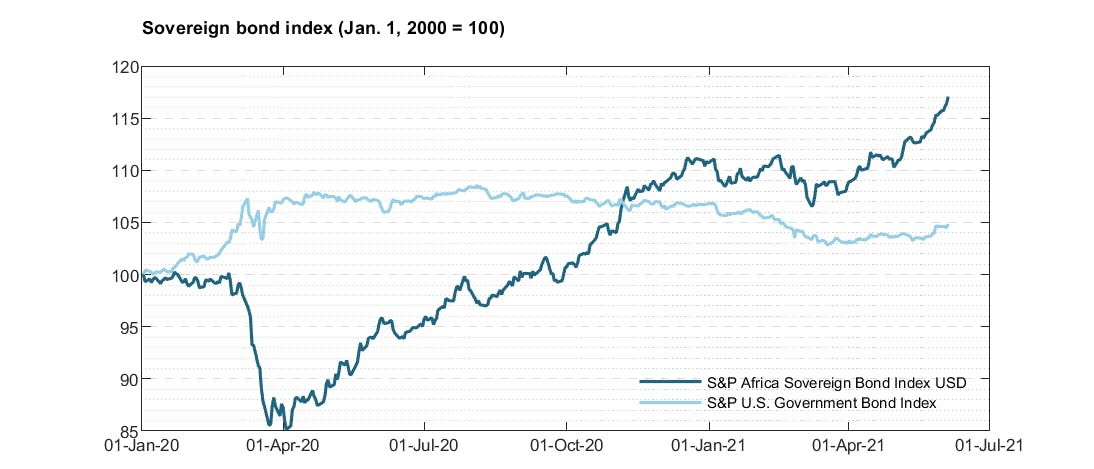

While the IMF became more optimistic about advanced economies in its April World Economic Outlook (WEO) update, it also left its weak African growth forecast almost unchanged. Even so, African bond prices have surged, and foreign currency government bonds have returned 5% so far this year (see Chart 1). Indeed, such bonds have returned over 20% to investors in the past 12 months compared to negative returns on US government bonds, with Angola and Zambia’s returning over 10% and 20% so far this year, respectively. Most African bonds have traded above par, representing an impressive financial recovery.

After African sovereigns took the brunt of COVID-related rating downgrades in 2020, their overall rating momentum this year remains profoundly negative, with downgrades outnumbering upgrades by five to one in the first quarter. Even so, some African ratings began to creep back up in early 2021. Moody’s raised Benin’s rating to B+ in early March before Fitch improved its rating outlooks for both Benin and Cameroon.

Even some bond issuance has returned after drying up entirely between March and November 2020, when Cote d’Ivoire became the first Sub-Saharan government to issue (at €1 billion over ten years) since the pandemic began. Benin followed in January 2021 (€1 billion), extending its euro-yield curve to an unprecedented 30 years. Both sovereigns have credit and debt ratings that are far above average compared to their African peers, and each of their bond issuances was heavily oversubscribed, as was Senegal’s in €775 million (2037) issue in early June.

Ghana — a country with a relatively stretched government balance sheet — followed suit in March, becoming the first sub-Saharan African sovereign to issue a Eurobond in US Dollars since COVID-19 went global and the first African government ever to issue a zero-coupon Eurobond. With no interest due until maturity in 2025, such a structure will help the Treasury push its debt service costs further into the future — a move that was widely praised for its innovation. That said, it may just as well be a sign that Ghana’s debt-servicing capabilities will be somewhat impaired in the coming years, as reflected in its low ‘B-’ ratings from Moody’s and S&P. The zero bond’s yield premium of 100 basis points also seems to indicate vulnerability. And yet, Ghana has announced another return to the Eurobond market to fill the increasing gap in its fiscal accounts. The West African nation is planning to raise as much as $1 billion by selling sustainable bonds, including Africa’s first social debt to fund a flagship policy designed to broaden access to education. Premieres galore in Ghana — the current superstar of frontier investors.

All that glitters is not gold

Despite the soothing calm and palpable enthusiasm of the African debt market, it may yet be treacherous. For a start, in Africa and elsewhere, the problems of debt overhangs in developing countries remain unresolved. Indeed, while 30 Sub-Saharan African sovereigns (80% of all eligible countries in the region) have participated in the G20 debt service suspension initiative (DSSI) introduced early in the pandemic for debt owed to official creditors, only Chad and Ethiopia have requested a debt ‘treatment’ (a.k.a. restructuring) under the common framework.

The rest have opted to kick the can down a road that the G20 has decided will end on 31 December 2021, when the DSSI is scheduled to be discontinued. Not only will DSSI savings no longer accumulate, but the debt service payments that were suspended during 2020 and 2021 will also need to be made from 2022 on a schedule that has yet to be determined. And these suspended payments could be significant. For example, the IMF estimates that Angola’s could amount to over $3 billion (or 3.3% of GDP), Kenya’s over $1 billion (1.4% of GDP) and Ghana’s more than $500 million (0.9% of GDP).

African governments’ deep-rooted reluctance to clear the decks is driven by a fear that debt restructuring and the concomitant declaration of a technical default by the rating agencies would prevent them from accessing capital markets for extended periods and make them pariahs in international finance. This concern is understandable, not least because some creditor representatives are actively promoting it. Nonetheless, the fear is unfounded. Logic and ample precedent suggest that a restructuring would improve sovereigns’ balance sheets and creditworthiness, enabling them to access capital markets sooner and on better terms.

This is all the truer in an environment where global liquidity remains bountiful and interest rates for highly rated debt are at rock-bottom, notwithstanding some signs of life in the US Treasury market earlier in the year. Investors will also appreciate that African nations’ need for restructuring emerged not from persistent Argentina-style economic mismanagement, but as collateral damage of the most dramatic global economic shock in living memory. In this context, requests for debt restructuring won’t be viewed as a precursor of future defaults.

Still, not a single restructuring has been concluded. Not even Zambia appears to be close to a breakthrough. Zambia was in debt distress well before the pandemic and was trying to avoid becoming the first African sovereign to default in the COVID era until it missed a Eurobond payment in October.

Bond buyers seem to be interpreting the absence of debtor demands for restructuring as a positive sign. But then again, we may be enjoying a brief period in the tranquil eye of a storm that has yet to dissipate. If so, the current dearth of debt restructurings may not last. According to the IMF, six low-income Sub-Saharan sovereigns were already “in debt distress” at the end of April 2021 (only one country outside Africa, Grenada, is also in distress). A further thirteen Sub-Saharan sovereigns are at a “high risk” of debt distress. And only two, Tanzania and Uganda, are deemed to be at “low risk” (compared to eight countries outside Africa).

African credit metrics aren’t encouraging

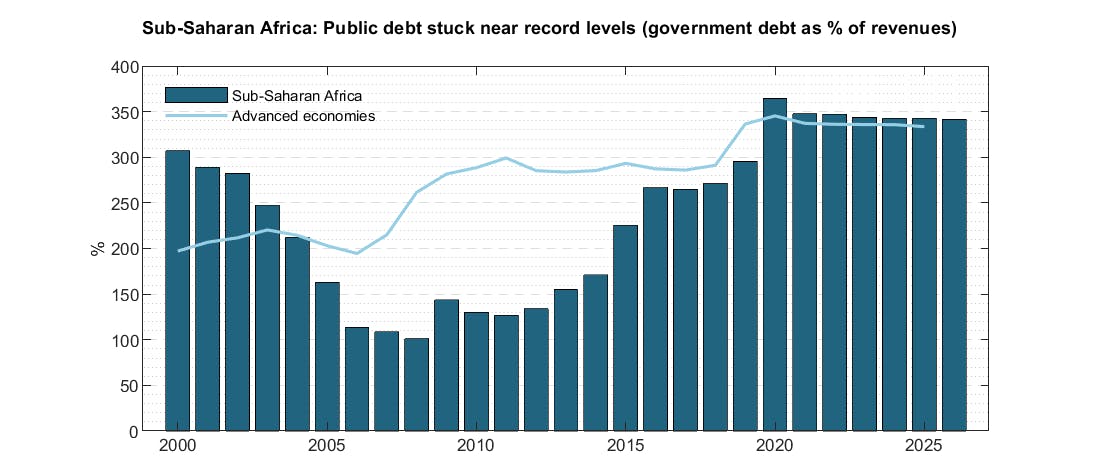

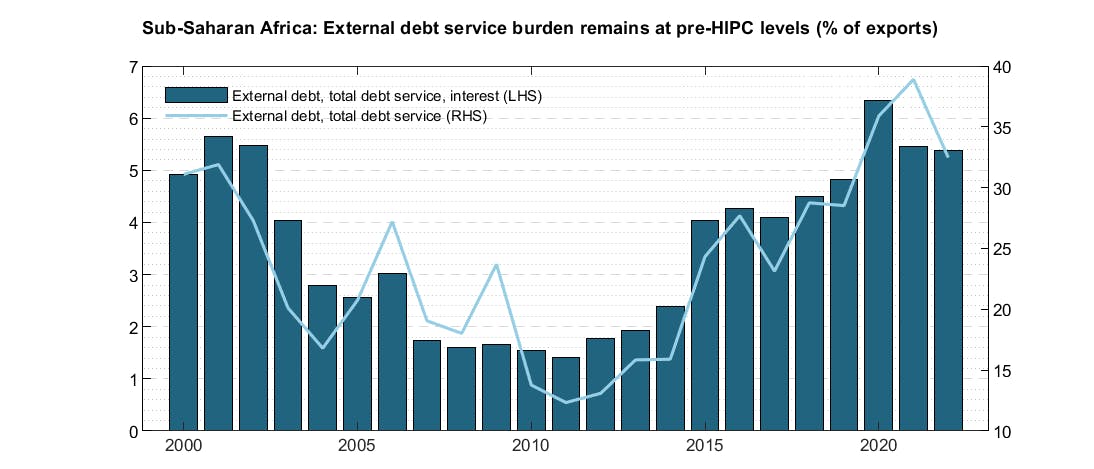

Charts 2 and 3 show that different debt burden metrics reflect the financial precariousness of African governments. On average, debt and debt service costs are where they stood at the beginning of the century, when the Heavily Indebted Poor Countries (HIPC) initiative reduced debt overhang in a purposeful and comprehensive debt relief effort — and did so in a much more benign global economic environment. More than half of the debt increase since then preceded the pandemic. Leverage really took off after commodity prices fell and the world’s leading central bankers implemented hyper-stimulus in the mid-2010s, which made foreign borrowing easy even for low-rated frontier sovereigns hit by a nasty terms of trade shock.

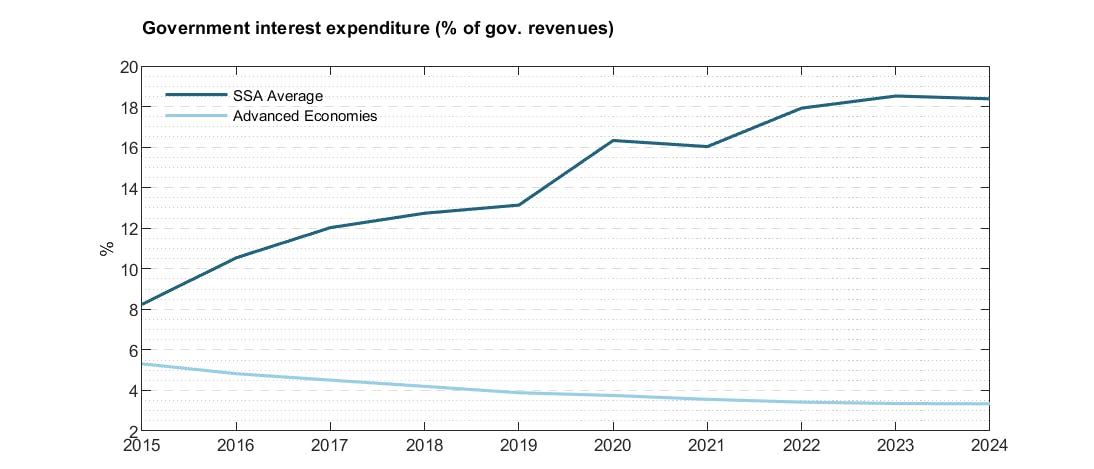

As a share of revenues, African countries now have a higher debt load than the far more resilient and richer advanced economies (Chart 2). And the bad news doesn’t end here. As Chart 4 shows, the interest burden of 18 rated Sub-Saharan African sovereigns has more than doubled since 2015 even as it dropped by over a third in advanced economies, according to data from S&P. As a share of government revenue, African nations now need to stump up more than five times more than advanced economies, up from “only” 1.6 times as much in 2015.

And this is only the average. Some individual sovereigns must divert even more of their scarce government resources to debt service, with five countries spending over a quarter of their budgets on interest alone (in descending order: Ghana, Zambia, Angola, Nigeria and Kenya). The average interest-to-revenue ratio increased on the continent by almost 10 percentage points between 2015 and 2022, and by more than 25% for the first three of the sovereigns mentioned above. All S&P-rated African sovereigns saw their interest burden go up except for the Democratic Republic of the Congo, where the interest ratio declined by a marginal 0.1% of revenues. The contrast with advanced economies could not be more stark. Here, the government interest-to-revenue ratiofellby a third to only 3.3% of revenue on average, with only Israel and Japan logging (small) increases.

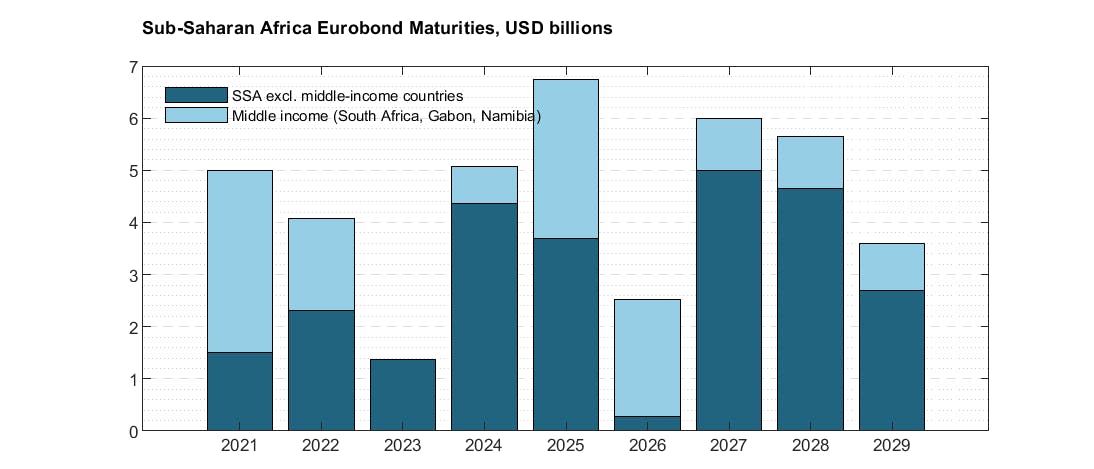

The fact that relatively few sovereign Eurobonds issued by low-income governments are maturing in the near term may also work in favour of African debt markets this year, as this implies that comparatively little new issuance is needed to roll over bonds coming due. While next year will see a modest increase in maturities, crunch time will arrive in 2024 (see Chart 5). If no solution to the debt overhang is found by then, expect distressed debt exchanges to become more common.

Our ratings signal caution

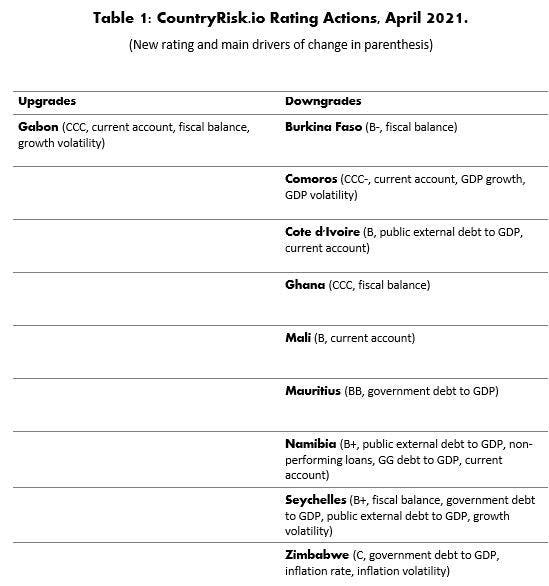

At CountryRisk.io, we assign risk scores and derived ratings [1] for 46 Sub-Saharan African sovereigns. The April revision of the IMF’s World Economic Outlook forecast led us to change ten African ratings. Of those, only one — Gabon — was an upgrade, as the nation benefitted from an improved oil price outlook, at least for now. Meanwhile, we reduced the ratings of nine African sovereigns, including Cote d’Ivoire, Ghana, and Namibia (for a complete list, see Table 1). This made Sub-Saharan Africa the region with the most negative balance of CountryRisk.io ratings revisions.

Although the pricing of African Eurobonds suggest that the mood has improved, the data have not. Indeed, in many cases, credit metrics have deteriorated further. As table 1 shows, weaker African data has been concentrated in public debt metrics, the fiscal balance and, in some cases, weaker current accounts. Neither a bond rally nor a temporary debt service relief changes the fundamentals. As such, we believe that most of the work needed to reduce risks and repair balance sheets still lies ahead.

[1] Although we use standard rating symbols for comparability, the sovereign risk scores we generate using our analytical algorithm are not ‘ratings’ in the regulatory sense. We do not hold a ratings license and have no intention of applying for one.