Taking the pulse: sovereign ratings during the pandemic

A little more than a year ago, on January 30, 2020, the World Health Organization declared COVID-19 to be a “Public Health Emergency of International Concern”.

Dr. Moritz Kraemer

Mar 16, 2021

A little more than a year ago, on January 30, 2020, the World Health Organization declared COVID-19 to be a “Public Health Emergency of International Concern”. By March 11, the WHO had designated COVID-19 as a pandemic—one that would go on to precipitate the most severe peacetime recession since the Great Depression.

The OECD estimates that the global economy shrank by 3.4% in 2020. This was by far the most significant contraction in living memory; even 2009, the nadir of the global financial crisis, saw the world’s economy shrink by just 0.1%. According to the IMF’s estimates the slump was twice as large in so-called advanced economies (AE, -4.9%) than it was in emerging markets and developing economies (EMDE, -2.4%, all country group definitions follow the IMF classification).

AEs will only collectively regain their pre-pandemic level of economic activity towards the middle of 2022. Some economies, such as the euro area, will not break even before the end of that year, with several countries (including France, Italy, and Spain) taking even longer than that. Meanwhile, among EMDE countries, heavyweights such as Mexico and South Africa will have to wait until at least 2023 for their economies to rebound to where they were in 2019. Most EMDEs are expected to catch up faster than the typical AE. Once you factor in the uncertainty around those forecasts and some potential downside risk, several countries—both rich and poor—could end up seeing at least half a decade of lost economic growth; a toll exceeded only by the loss of human well-being and lives.

Public debt has spiraled

S&P Global calculated that net commercial borrowing by sovereigns reached USD 10 trillion globally in 2020 (including the change in short-term debt). While that number is expected to gradually drift back down, this year’s sovereign net long-term issuance will remain 2.5 times higher than pre-COVID levels. In 2020, government debt ratios in advanced economies surged by 20 percentage points to 124% of GDP, a level the IMF estimates will remain unchanged until at least 2025. In EMDEs, debt ratios remain at less lofty levels, collectively rising “only” nine percentage points to 61% of GDP last year—the first time that the debt ratio for this group has broken the 60% threshold. The IMF also predicts that EMDE public debt will rise even further, hitting almost 70% by 2025.

All things considered, then, COVID-19 has posed an unprecedented negative shock to governments’ creditworthiness. Notwithstanding the human calamity and economic turmoil caused by the coronavirus, the crisis has afforded us a rare glimpse into how sovereign rating agencies behave when a sudden and unexpected storm hits every country at once. To get a handle on this, we examined the rating behaviours of the three dominant rating agencies: Moody’s, S&P and Fitch (the “Big-Three”). In assessing the “ratings reaction function”, we analysed all rating actions during the period in which the brunt of the impact was felt: from January 31, 2020 to February 28, 2021.

Poorer countries more exposed to downgrade

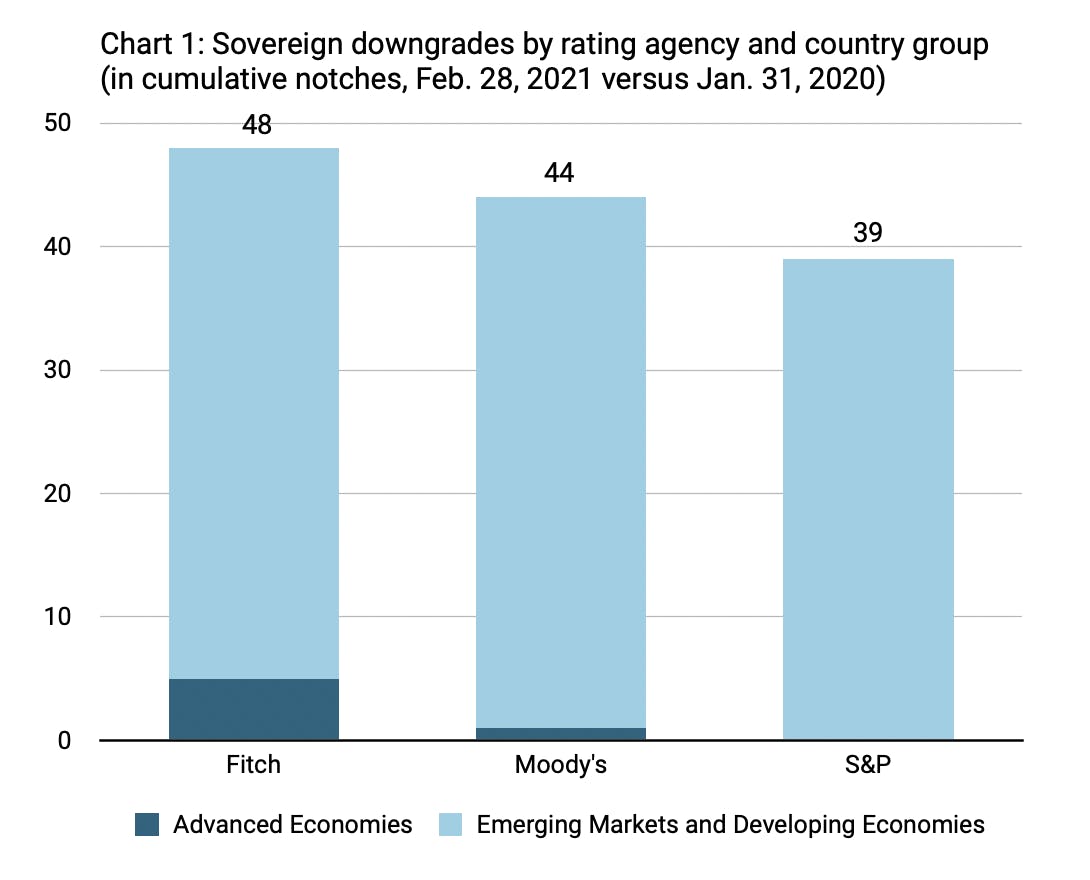

When we compare the sovereign ratings by the Big-Three at the end of that period with the starting rating, we find that 48 sovereigns had seen their rating cut by at least one agency. Half of those sovereigns experienced more than one downgrade. Fitch was the most active, with 45 downgrade episodes (or 26% of the sovereigns it rates), followed by S&P (37, or 18%) and Moody’s (33, or 20%).

Chart 1 shows the rating downgrades in cumulative notches (since there have been several multiple notch downgrade episodes, the numbers differ from the number of downgrade episodes referred to in the previous paragraph). The first observation we can make, with even a cursory analysis, is that the agencies seem to have largely spared AEs from downgrades.

Although, as shown above, the economic fallout from the virus was more severe in AEs they experienced only six notches of cumulative downgrades (or 4.6% of all downgrades). This is a stark contrast to the 29% share of AEs in the totality of all Big Three issuer ratings. Except for the U.K.-downgrade by Moody’s, all other AE-downgrades were by Fitch (Canada, Italy, U.K., Slovakia, and Hong Kong). That is all. Meanwhile, S&P has not lowered any AE sovereign rating since 2017 and, alone among rating agencies, did not do so in 2020. In fact, the agency evenimprovedits rating outlook for Italy, one of the countries hit hardest by the pandemic, from negative to stable in September 2020. The agency’s only positive outlook going into 2021 was for New Zealand (also an AE), which was eventually upgraded in February 2021. Looking ahead, S&P assigned just three (Australia, Slovakia, and Spain) of its 27 negative outlooks to AEs. Therefore, we should expect the relatively strong ratings resilience of AEs to remain in place during 2021.

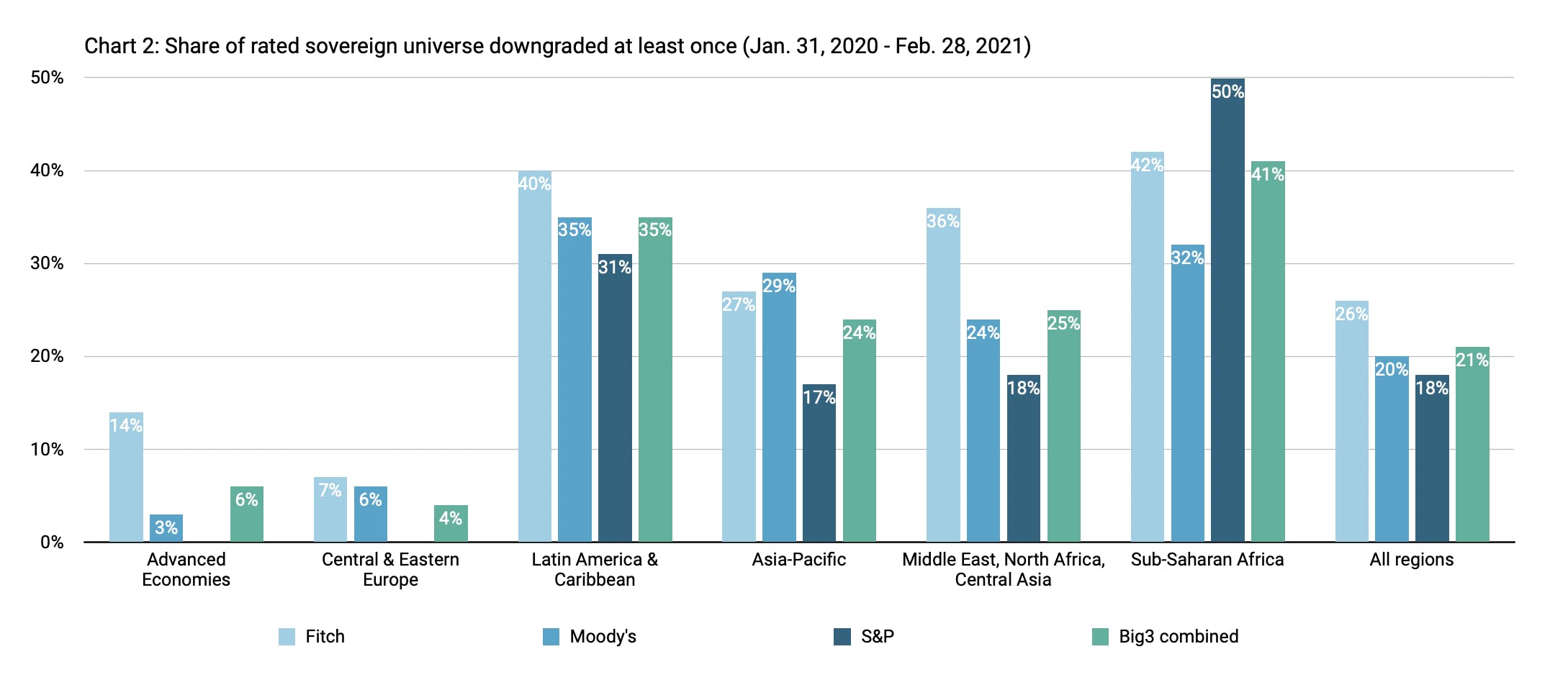

EMDEs did not fare so well. Chart 2 displays the share of each agency’s portfolio of rated sovereigns that was downgraded by at least one notch. Sovereigns in Sub-Saharan Africa (41%) and Latin America and the Caribbean (35%) were most likely to be downgraded.

Non-AE Central and Eastern Europe (CEE) includes several economies, especially some EU members, that are close to being considered AEs. Like AEs, that region, too, was almost entirely spared: Moody’s lowered Turkey’s rating and Fitch downgraded Armenia. S&P took no action in the region. Fitch was the most severe agency in almost all regions. S&P was the ratings firm offering most forbearance, except in Sub-Saharan Africa, where it was the downgrade leader, lowering the ratings of 50% of sovereigns in the region.

What explains these inter-regional differences? One could argue that rich, diversified countries are more resilient to shocks than poorer, more vulnerable economies. That is undoubtedly true. However, it is also true that the shock delivered by COVID-19 was not evenly distributed across economies. In fact, the hit to growth and public debt accumulation has been twice as large for AEs than for EMDEs, not to mention their significantly larger death tolls. Given that context, it is not at all clear why rich countries’ ratings remained largely untouched even as their poorer peers were subject to more extensive downgrades. More analysis is required to solve this puzzle.

Early action, but no second wave

With the quality of a rating signal being significantly dependent on its timeliness, the overwhelming speed at which the virus spread across the globe last spring made it critical for agencies to reassess their ratings just as quickly.

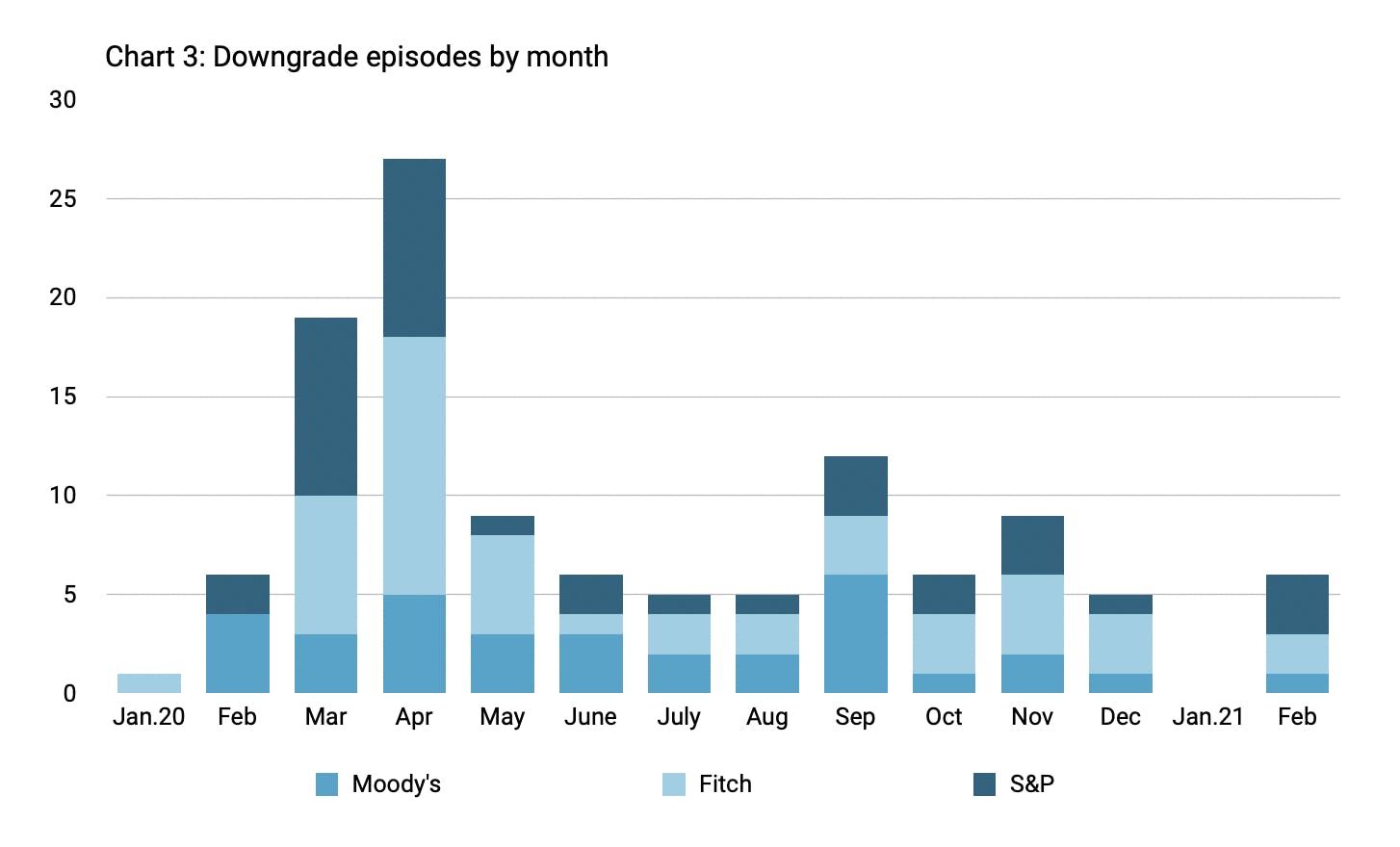

Chart 3 reveals a flurry of downgrade activity during March and April 2020, especially by Fitch and S&P.

After that, the pace became somewhat more leisurely, which may have been partly due to the gradual (albeit, ultimately, temporary) retreat in the number of COVID cases. As the northern summer ended, downgrade activity picked up once more, especially by Moody’s. However, when the second wave began in Q4 and forced governments to declare renewed lockdowns and stimulus spending, downgrade actions did not surge in tandem. In January 2021, when much of the world was in the grip of the second wave, not a single rating was lowered.

For the time being the agencies were largely done, possibly due to hopes for a quick recovery following a successful vaccination drive. That said, the continuance of negative outlooks, especially on the ratings of EMDE sovereigns, suggests that ratings agencies see a relevant risk of further ratings erosion.

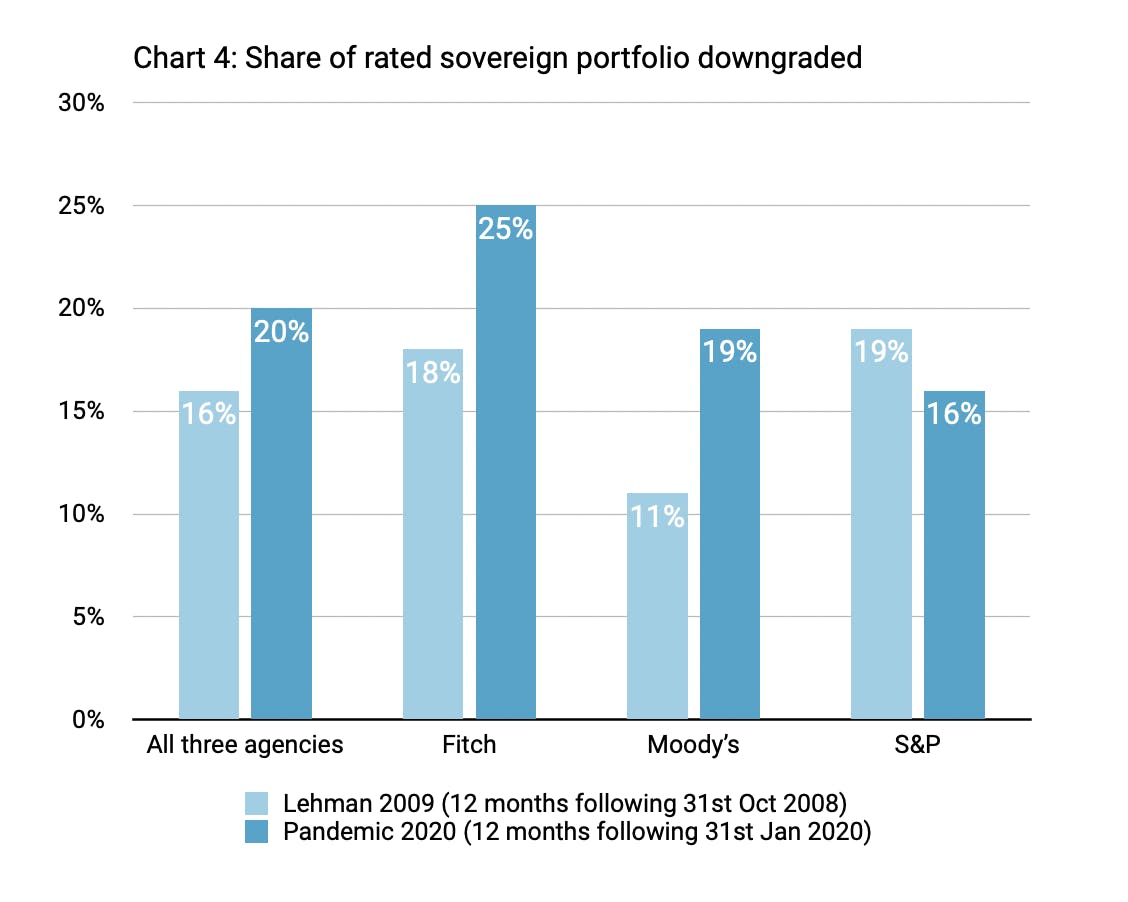

Fitch and Moody’s reacted stronger during the pandemic than following the Lehman crisis.

The seasonal profile of downgrades appears to align with the speed of the virus’s spread last spring. Yet, to us at CountryRisk.io, the overall reaction to such a profound weakening of credit fundamentals seems surprisingly mild. To assess the accuracy of this view, we contrasted rating agencies’ behaviour in 2020 with that of the 12 months following the collapse of Lehman Brothers (October 2008 – October 2009). As shown above, though still severe, the global recession back then, as well as the resulting blow to public finances were still vastly milder than what we saw in 2020. Therefore, one would also expect rating actions to have been comparably less dramatic.

To ensure a like-for-like comparison between the Lehman and COVID shocks, we need to account for the much larger sovereign ratings universe that has emerged in the years since the former crisis. As such, it would be inappropriate to simply compare the number of rating actions that followed the collapse of Lehman Brothers with the number that occurred during the pandemic. So, to reflect the increased number of rated sovereigns, we put the downgrade count into relation with the number of rated sovereigns for each agency and episode.

Chart 4 contrasts the two episodes. Overall, the Big-Three have lowered a larger share of their rated portfolio during COVID-19 than at the height of the financial crisis (20% versus 16%).

Both Fitch and Moody’s have taken more negative actions than following the collapse of Lehman and during the crisis that ensued. In the case of Moody’s this may partly reflect the observed wait-and see-attitude it had assumed during the initial stages of the global financial crisis. S&P had been the most downgrade-inclined agency during the financial crisis but became the most lenient during the COVID episode. Indeed, in a notable contrast with its competitors, S&P downgraded a lower share of its rated portfolio in 2020 than in 2009.

CountryRisk.io signals a more significant increase in sovereign risk.

In contrast to sovereign ratings issued by the established agencies, CountryRisk.io’s sovereign risk scores rely exclusively on quantitative analysis with no discretion applied by analysts.[2] Despite using standard rating symbols for comparability, the sovereign risk scores generated by our analytical algorithm are not “ratings” in the regulatory sense. CountryRisk.io does not hold a ratings license and has no intention of applying for one. What it does offer is a quick reassessment of risk as the data change.

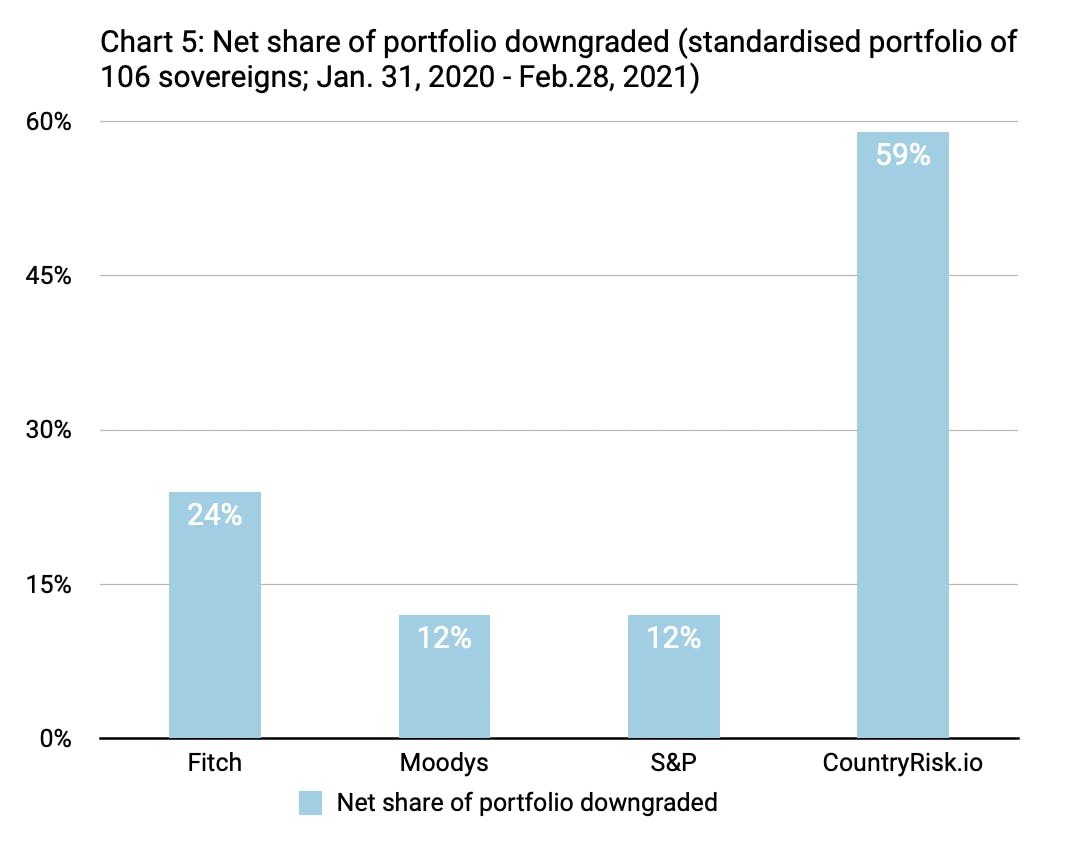

Chart 5 shows that during 2020, CountryRisk.io adjusted many more “ratings” than the traditional agencies.

The bars display the net downgrade ratio between January 2020 and February 2021, applied to a standardised sovereign portfolio rated by all three agencies (n=106). This allows for a like-for-like comparison between those agencies and CountryRisk.io. The number of sovereigns downgraded is corrected by the number of upgrades that have occurred during the same period. The derived net downgrade ratio amounted to 12% of the portfolio for S&P and Moody’s, and around twice that for Fitch. Meanwhile, the algorithm applied by CountryRisk.io generated a net downgrade rate of over half the entire portfolio.

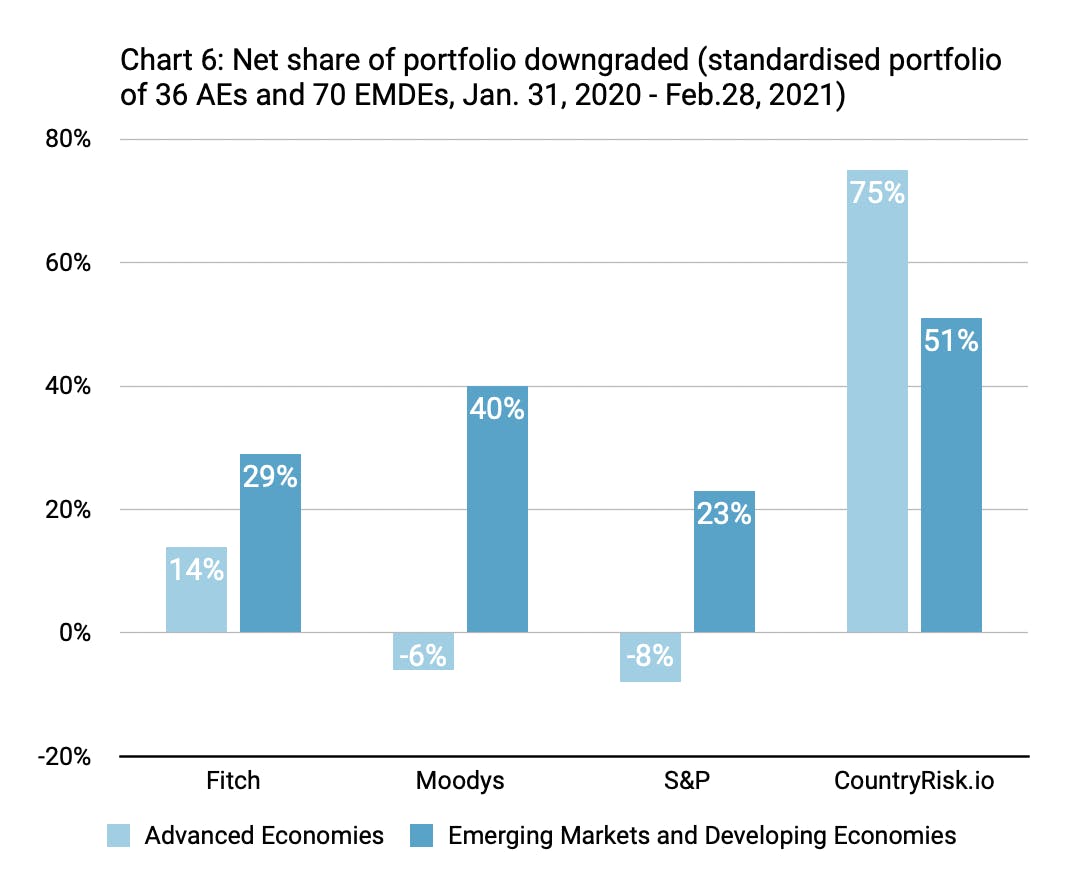

Once again, it is interesting to distinguish between rich and poor countries. On the standard sample of 36 advanced sovereigns, the net downgrade ratio of CountryRisk.io was 75% (see Chart 6). In other words, the net downgrade ratio for advanced economies was more severe than for emerging and developing sovereigns (51% of a standardised portfolio of 70). This is in line with the observation that, by and large, the pandemic more severely impacted advanced economies.

Chart 6 shows the opposite pattern in the rating actions of the agencies. Taking the three agencies together, the net downgrade ratio for advanced economies during the pandemic was zero.

S&P and Moody’s even displayed net upgrades for advanced economies (S&P upgraded Latvia, Lithuania and New Zealand and downgraded none; while Moody’s upgraded Greece, Lithuania, and Slovenia and downgraded the UK).

What could be the reasons for the different outcomes when comparing CountryRisk.io’s automated rating scores with ratings conducted by agencies?

One reason may be that the agencies viewed the pandemic as a transitory shock: most countries’ medium-term credit fundamentals remained unchanged. Therefore, in line with the philosophy of “rating through the cycle”, perhaps agencies saw less need to react.

Some analysts have also stressed the importance of hyper-accommodative monetary policies for public debt sustainability. Indeed, despite the increase in debt burden, the interest burden for many countries has shrunk. But implicit to this argument is the view that the current monetary stance will be maintained throughout the time horizon of a sovereign rating, which agencies typically define as up to 10 years for investment-grade issuers. That is a bold call on monetary policy. To suggest that central banks will force rates to remain at current levels for a decade assumes not only that they are able to do so, but also that the real economy will remain in crisis mode through to 2030. That scenario would not bode well for sovereign ratings. Only an environment of sustained low real interest rates and a simultaneous economic recovery would justify the absence of a more robust rating reaction for advanced economies.

Rating agencies are now much more closely supervised than they were over a decade ago, which may have led agencies to be more cautious with sovereign downgrades. For example, Steven Maijoor, chair of the European Securities and Markets Authority that supervises agencies in the EU, reportedly warned against “knee-jerk” downgrades. Instead, the agencies should time any downgrades in an “appropriate way”. Such regulatory “guidance” did not exist in 2009.

Furthermore, the fact that rating analysts of several agencies were tried (and later acquitted) in an Italian criminal court for rating downgrades during the eurozone crisis may have also affected recent decision-making, if only subconsciously. The observation that most of the analysts that had been accused were from S&P could provide clues for the relatively more cautious rating approach of that agency during the pandemic, especially towards advanced economies. As does the fact that S&P, alone among rating agencies, had been sued by the U.S. Department of Justice in 2013. Although sovereign ratings were not the underlying reason for the case brought against it, S&P said at the time it considered the lawsuit as “retaliation” for having stripped the US of it’s ‘AAA’-rating two years earlier.

Where does this leave us?

Reasonable people can argue about the appropriateness of rating levels or actions. They always have. And, since ratings are opinions about the future, they always will. This is a normal and entirely healthy analytical debate. That said, it does look as though rating agencies’ overall reaction (perhaps except for Fitch) has been surprisingly mild since the onset of the COVID-19 pandemic. This observed hesitancy around ratings downgrades being particularly pronounced about advanced economies. We conclude that rating committees’ discretion has been overwhelmingly applied to the upside, keeping an otherwise looming wave of downgrades in check.

It is too early to judge whether the reluctance of raters to downgrade was the right analytical call. Indeed, there are plausible scenarios in which the pandemic ultimately leaves the creditworthiness of advanced sovereigns largely unscathed. Others will argue that such forecasts privilege hope over experience. Only time will tell. And of course, students of sovereign risk must not overlook the mounting pressure that ageing societies will pose on public finances.

What we consider somewhat unsettling, however, is that all three dominant agencies appear to have based their recent approach to sovereign ratings on comparably optimistic assumptions. This is particularly true for the two largest agencies — Moody’s and S&P — regarding advanced economies. As such, the variety and competition of credit views in the world’s largest asset class appears to be astonishingly limited. Since many investors must at least partly follow these agencies’ ratings, the lack of diversity may yet create investment risks should the agencies conclude that their hitherto optimistic outlooks need to be revised. What now looks like a downgrade trickle may yet become a torrent.

[1] The different proclivity for downgrades across agencies is unrelated to the average level of the rating. On January 31, 2020, before the spread of COVID-19, the average rating of the 106 sovereigns rated by all three agencies were all halfway between BBB and BBB- and statistically indistinguishable. S&P’s average rating was one-thirteenth of a notch lower than Fitch’s and one-fifth of a notch lower than Moody’s.

[2] CountryRisk.io’s sovereign rating model, which follows a scoring framework, considers both quantitative and qualitative indicators to capture a more comprehensive perspective of a country.