InsightsIreland: The emerald island has a green bond

Ireland: The emerald island has a green bond

In October, Ireland issued a so-called green bond for EUR 3bn, a first for the country.

Bernhard Obenhuber Dec 19, 2018

In October, Ireland issued a so-called green bond for EUR 3bn, a first for the country. A green government bond raises money that is earmarked for climate, environmental and social projects. Such bonds are also referred to as climate bonds, and by all accounts, are still a rare breed among government bonds.

Ireland is now a member of a still very small group of countries that has issued such bonds. The detailed description of the Irish green government bond can be found here. It includes the investor presentation, second-party opinion from Sustainanalytics and the underlying Green Bond Principles 2018 by the International Capital Market Association.

A short history of green bonds

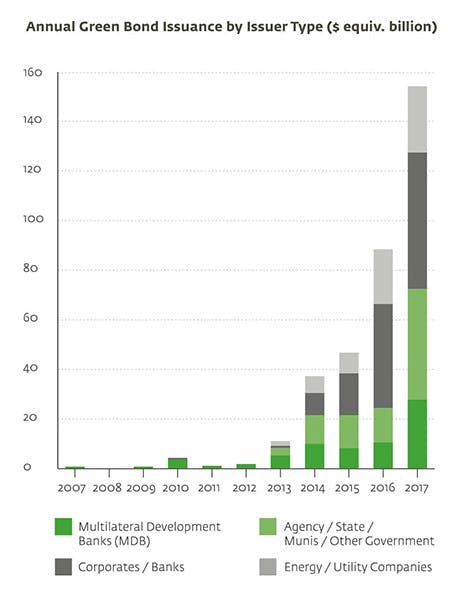

Green bonds have been around for roughly a decade. The European Investment Bank is credited with kicking off the green bond market in 2007 with an issuance that focused on renewable energy and energy efficiency. This transaction was followed by several bonds by the World Bank and other multilateral development banks. More recently, corporates and private sector financial institutions have also entered the market. In 2017, roughly USD 155bn of green bonds have been issued.

In the area of government bonds, Poland was the first country to issue a green bond. France, Belgium, Indonesia, Lithuania, Fiji and Nigeria have subsequently followed. However, with only USD 25.5bn of green government bonds having been issued so far, this constitutes just 0.1% of the total outstanding global (central) government debt. Hence, it’s still a long way to go before green bonds become a meaningful part of sovereign bond markets. While we discuss green bonds here, one should not forget that there are also social (impact) bonds that only differ regarding where the money is invested (e.g. affordable housing).

Doing good with your money

The money raised with the Irish green bond is earmarked for project financing of certain categories such as sustainable water and wastewater management, clean transportation or renewable energy. In addition, there is a list of excluded activities, among them the usual suspects like fossil fuel power generation, nuclear power generation or alcohol, weapons, tobacco, gaming, or palm oil industries. The detailed list can be found here.

So, given the broad range of eligible projects, it will be quite easy to allocate the green bond money. The exclusion criteria are also not very surprising or restrictive but nevertheless it will be more difficult for such “brown” projects to get funding in the future. The incentives should foster a more sustainable development in the future. In our view, the steering effect is the most important aspect here.

Transparency and accountability

Importantly, the green bond principles require that Ireland reports on the actual projects funded and their impact towards promoting sustainability. Accountability and transparent reporting will be a key aspect to make green bonds credible and to some extent also comparable to investors. This touches on the points raised by Steve Freedman in the recent interview.

As a bond investor, not only do I want to select the investment based on the eligible project universe that is aligned with my values and investment criteria, but I also want to track the non-monetary benefits over time (e.g. amount of CO2 reduced, affordable housing built,…). Unfortunately, Ireland will only report impact indicators every other year. In our view, countries should take the opportunity and engage in a meaningful dialogue with sustainable finance investors, as well as with the general public, about the project selection and monitoring of impact on ESG criteria.

Green bond ESG risk triangle: Bond structure, use-of-proceeds, issuer-risk ESG rating

One should look at ESG risk aspects of green bonds from three dimensions.

The first dimension should typically focus on the assessment of the overall bond structure, its features and whether it is in line with governance standards. Within the green bond segment, the Green Bond Principles 2018 by the International Capital Market Association have become the widely-followed standards. Another quality check could be if an independent committee evaluates the eligible projects.

Secondly, since the use-of-proceeds assessment focuses on the analysis of the funded projects and their positive environmental impact, we need to ask ourselves: Is the money really spent on the stipulated areas? How much CO2 was saved? And the like…

Thirdly, an important risk aspect is the analysis of the bond issuer. Here one should focus on the assessment of the state of the environment (e.g. share of protected areas) and environmental policies (e.g. incentives for renewable energy). Part of such an assessment is also if the country has a funding strategy that includes green bonds. We will cover this aspect in more detail below and apply it to Ireland.

Risk & return

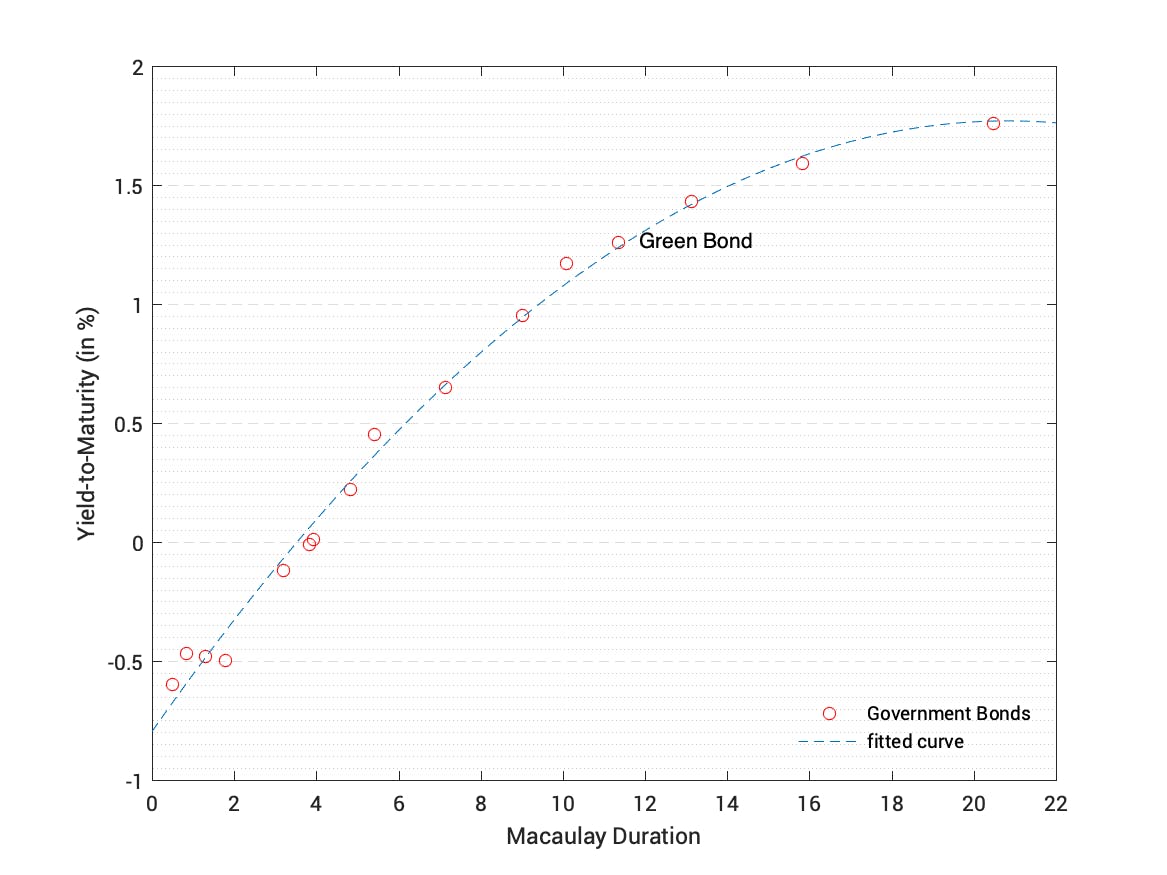

In terms of (credit) risks and returns, the Irish green bond has the same profile as any other Irish government bond. The green bond framework stipulates that the bonds rank pari passu with each other and with other Irish government bonds. So, if Ireland defaults on standard bonds, it will also be in default for the green bond. Same risk. This is clearly different in the case of project or revenue bonds where the return and the risks are clearly linked to a specific project.

The Irish green bond is currently trading at a yield-to-maturity of 1.26% as shown in the chart below. Overall, the bond trades very much in line with its peers (see Irish government bond curve below). It is too early to see if green bonds will see a more favourable demand picture in the future that could lead to a situation where green bonds trade at a lower bond yield than traditional bonds. As the credit risk is the same across bonds, the yield difference will likely be very limited.

Overall, you get the same return as with comparable government bonds and the benefit of knowing that your money did not finance a nuclear power plant.

ESG country rating

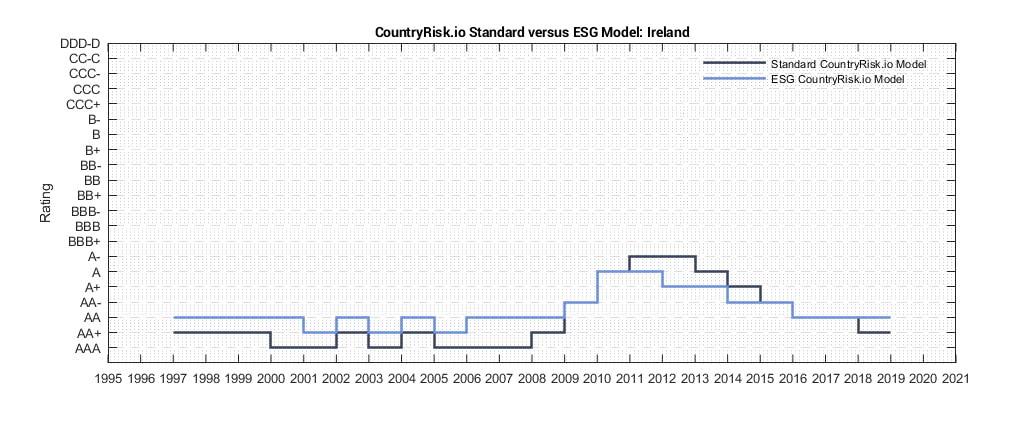

Given that all Irish government bonds have the same credit risk, we wanted to know what a fair credit rating for Ireland would be. Additionally, we asked ourselves if an assessment that only takes into account standard economic and financial indicators would differ from one that also looks at environmental, social and governance (ESG) factors.

Our quantitative country risk model for Ireland derives two ratings. The ESG sovereign risk rating is a “AA” on the common rating scales. The standard risk rating, which does not take environmental or social factors into account, is one notch higher at “AA+”. Ireland is currently rated by the credit rating agencies as A+ / A2 / A+ (SP / Moody’s / Fitch). In a nutshell, our quantitative rating model takes a more positive view on Ireland.

Comprehensive view: ESG CountryRisk.io platform

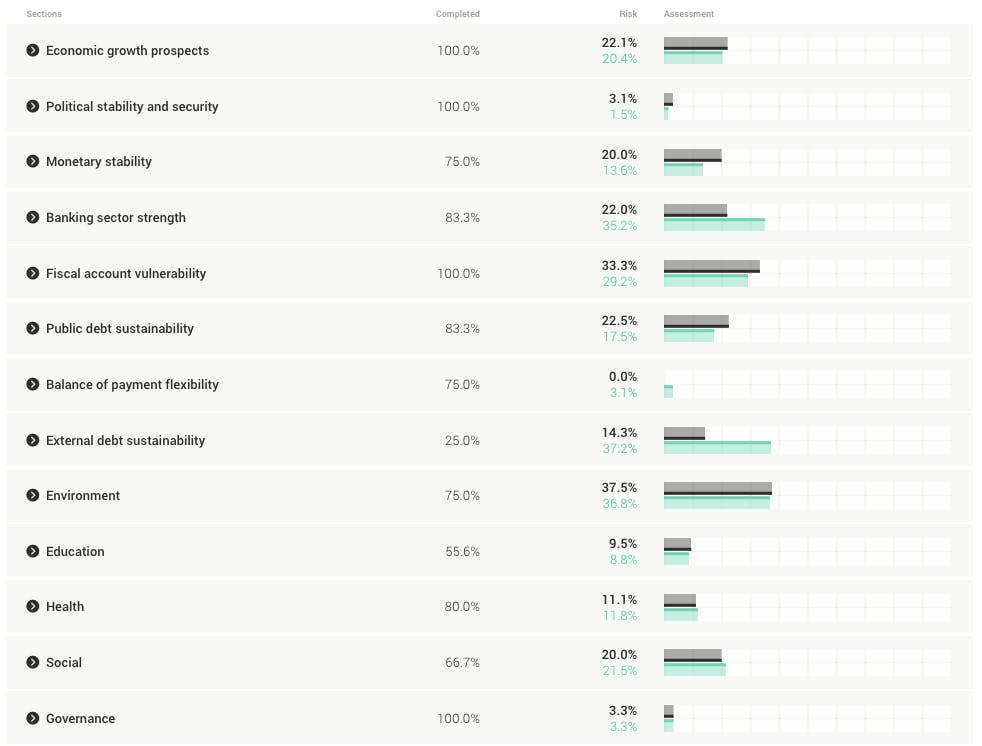

While our quant scores are very useful to monitor ESG risks across many countries, we find that a holistic analysis should also take into account a wide range of qualitative factors. Such an analysis can be done using the CountryRisk.io ESG analysis framework. It is a community-driven platform that allows the interested user to generate an ESG rating and to compare the result with the community average.

The overall outcome of my ESG rating assessment was a “AA-“ while another user rated Ireland at A+. This is a solid rating that indicates a low probability of default and reflects Ireland’s high degree of economic development. The open and transparent nature of the platform also enables me to easily identify the areas where Ireland performs well or where it still has some homework to do. Ireland scores highly in the areas of governance, education and health, but trails behind when it comes to social and environmental indicators.

The CountryRisk.io platform also allows you to compare your own assessment (the black bars in the screenshot below) with the community average (the green bars) across the various risk drivers.

Please join the ESG CountryRisk.io community and create your own assessment for Ireland or any other country that is of interest to you.

Outlook

We welcome that more and more countries issue green government bonds. While still a niche segment, it provides the right incentives, and as the market matures, investors will demand more transparency and accountability regarding the positive impact on the environment, climate and social aspects. On a macro level, the improved data availability and quality for tracking the UN Sustainable Development Goals are helpful. While on a micro or project level, we still need better standards that allow comparability across countries and projects.

The credit risk assessments of countries in terms of ESG risk factors are also still at an early stage. We at CountryRisk.io want to contribute by providing an open and transparent platform to enable anyone to conduct comprehensive due diligences and engage in a constructive dialogue with the community.

I want to extend many thanks to Jenny Asuncion and Steve Freedman for providing guidance and comments to this article.

About CountryRisk.io

CountryRisk.io provides free access to a comprehensive and transparent ESG country risk rating framework and country risk analyses. The CountryRisk.io rating platform is open to everyone. The platform also encourages the constructive exchange of findings and ideas among its users. As members of the CountryRisk.io community, we collectively generate multiple ESG rating views for a given country based on each individual’s fundamental analysis.

Join CountryRisk.io and make ESG sovereign ratings a public good: www.countryrisk.io