Spectacular busts in Argentina and Greece notwithstanding, sovereign defaults to commercial creditors have been relatively infrequent of late...

Dr. Moritz Kraemer Feb 09, 2021

Casa Rosada, Buenos Aires, Presidential Palace. Photo by Rafael Leao (Unsplash)

Spectacular busts in Argentina and Greece notwithstanding, sovereign defaults to commercial creditors have been relatively infrequent of late — indeed, for the last century. While such incidents were much more common up to the 1930s, the only significant wave of sovereign defaults since then started in the 1980s.

But as the COVID-19 pandemic sparked a new global recession and rating agencies busied themselves downgrading emerging market sovereigns, the specter of sovereign defaults returned. In 2020, sovereigns from Belize, Ecuador and Suriname in the Americas to Lebanon and Zambia in the Middle East and Africa defaulted on their bonds. And despite the country’s attempts to forge a new path, Argentina too was inducted into this unhappy club.

2021 is not shaping up to be much better. According to Goldman Sachs, Angola, Gabon, Iraq, and Sri Lanka are all highly likely to default this year. Given that the shadow ratings for these countries fall along the lower end of the sub-investment band, we at CountryRisk.io are in broad agreement with that assessment. Goldman Sachs also picked out Belarus, El Salvador, Mongolia, Mozambique, and Pakistan as potential default candidates in 2021, and warned that exceptionally high debts could precipitate restructurings that will be more severe than those to which investors are accustomed.

This rather cloudy outlook offers the perfect backdrop to revisit the issue of identifying reliable harbingers of sovereign defaults. Much of the discussion about creditworthiness in advanced economies has been framed around issues of government debt. But is a forecast of deteriorating public finances really a precursor to sovereign default? That is one of the questions we will be addressing in this article. (Spoiler alert: it isn’t!)

Economists and policymakers might consider a range of economic and financial indicators relevant to identifying growing sovereign credit risk, many of which may be informed by strong-held beliefs or ideologies. However, determining which economic trends lead to defaults cannot be a question of mere conviction, but rather one of empirical evidence. And it is such evidence, and what it enables us to infer about the predictors of sovereign defaults, that we seek to reveal here.

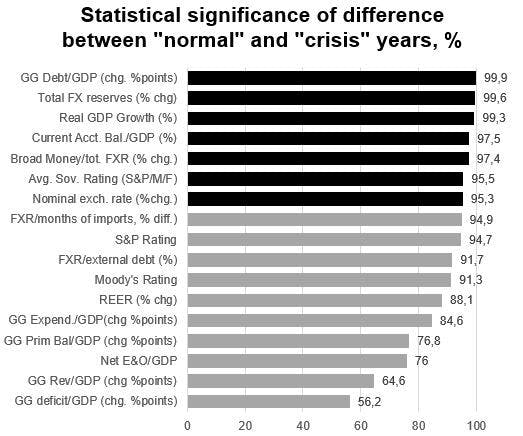

We analysed 134 sovereign defaults on commercial creditors between 1970 and 2017 using a statistical test to compare the means of 28 variables during crisis and non-crisis periods. Notably, many defaults occurred in the 1980s (45) and 1990s (39). We used the Bank of Canada/Bank of England Sovereign Default Database to identify relevant episodes.

The variables we chose are commonly referred to in the academic literature and/or credit reports from market analysts and rating agencies. To identify the variables that change systematically prior to defaults and, in turn, significant patterns that recur over time and between geographies, we compared the mean average of each variable in ‘normal’ years with those of ‘crisis’ years. We define ‘normal’ years as the years five and six prior to the default, and ‘crisis’ years as the two years immediately preceding the default, plus the calendar year in which the default occurred. (Since the default database only provides for the calendar year of the default, but no information about the month, we apply a reduced weight of 0.5 to the calendar year in which the default occurs. This reduced weight reflects the technical assumption that “on average” a default happens in the middle of the year).

The bar chart shows a selection of variables applied, indicating their predictive value. Each bar displays the significance (t-Test) of the difference in respective values during normal and crisis years. The number assigned to each bar is the statistical probability (in per cent) that the value of the indicator in question will be different in crisis years compared to normal years. Variables with at least a 95% probability are highlighted in black.

There are three key takeaways from this analysis.

1. Only a few variables are statistically significant.

Just seven of the 28 variables we analysed showed a statistically highly significant difference (defined as a probability that the value of the indicator will vary of 95% or higher) between crisis years and normal years, with the remaining three-quarters of the variables showing no such difference.

There are a few possible explanations for this:

a) Most straightforwardly, while the insignificant variables may have been relevant to some of the defaults we analysed, they nevertheless do not reflect a generalised pattern. As an aside, this shows the importance of using evidence over intuition to determine which economic trends are predictors of defaults — a small number of highly publicised defaults (such as those in Greece or Argentina) to which certain variables were specifically relevant can easily yet unduly influence our intuitions as to which variables are generally relevant.

b) A variable that is insignificant in isolation may interact with other economic or financial variables in a way that applies collective stress to sovereign credit.

A sovereign default is a complex event that rarely lends itself to mono-causal explanation, and a panel analysis like ours cannot replace a thorough case-by-case analysis of default episodes. Understanding how factors interact, then, may be critical to consistent default predictions. It is the capturing of this interconnectedness that is delivered by analytical models like the one applied by CountryRisk.io.

c) The data we used were not without challenges. First, default dates are only available by calendar year, making a precise classification of normal and crisis years (which lies at the heart of this analysis) more difficult.

Secondly, the quality of the data themselves may also leave something to be desired. Sovereigns that default are often characterised by weak institutions, which tend to be bad at collecting and processing economic data compared to those in more creditworthy countries. In addition, many defaults in the sample occurred in the late twentieth century when data in many countries were of a lower quality than they are today.

2. External risk variables are the best predictors of impending defaults.

Such variables include FX reserves, current account balances, reserve coverage of the monetary base, nominal exchange rate change, import coverage of reserves and external leverage.

In contrast, apart from the government debt ratio, we could not detect a significant difference in fiscal indicators between normal and crisis years. In fact, ratios such as fiscal deficits or revenues over GDP did not show any meaningful difference between normal and crisis years. Even rising public debt in the lead-up to a default is explained not by soaring deficits, but by currency depreciation caused by having a substantial proportion of foreign-currency-denominated sovereign debt. In short, the significant increase in government debt before a default is primarily caused by external stress, not fiscal slippage.

Defaults are, therefore, typically the result of balance-of-payments crises. Fiscal indicators weaken systematically only after the default: once the default happened, government deficits rise, and revenues drop sharply as the accompanying economic recession takes root. That said, fiscal slippage can coincide with such a crisis, or even help cause one where cross-border capital flows dry up out of concern around fiscal performance. While a sizeable fiscal deficit may be acceptable to investors in the context of a benign external environment, an external shock can cause investors to baulk even at the idea of maintaining such a deficit, let alone increasing it. Understanding the root causes of balance-of-payments crises, then, is a vital project to which a holistic analysis is essential.

3. By and large, lower credit ratings signal higher default risks.

We found a high probability that a sovereign’s rating will be lower in crisis years than in normal years. Of course, one could argue that this is the least we should expect from agencies — after all, producing ratings that indicate whether a default is likely is the industry’s raison d’être. But there is another, more nuanced, conclusion to be drawn here: rating agencies conduct holistic analyses that combine the various factors we have looked at in this article, potentially affording such analyses more predictive power than an analysis of any one of these factors ever could on its own. This belief has informed the design of CountryRisk.io’s comprehensive risk model.

With respect to the predictive value of ratings, another finding stands out: the average rating of all agencies is a better indicator of an impending default than a single rating of individual agencies. We believe this reflects the complexity and idiosyncrasies of each default episode and, therefore, that consulting multiple sources is valuable to the assessment of default risk. However, a dearth of competition in the rating industry limits the number of opinions available for aggregation. This makes it harder to predict defaults, especially if one believes that an agency’s rating is partly informed by those of other agencies. As such, allowing for the inclusion of independent risk assessments, as CountryRisk.io does, can generate more accurate default predictions.

So, where has our exploration of the candidate signs of an impending sovereign default taken us? On the one hand, our analysis suggests that we should pay particular attention to balance-of-payments crises. On the other, we have also seen that a range of different circumstances can lead to sovereigns defaulting on their financial obligations. As Tolstoy wrote in Anna Karenina, “All happy families are alike; each unhappy family is unhappy in its own way.” And just as any family counselor worth their salt must delve into the peculiarities of knotty relationships, so must financial analysts examine the idiosyncrasies of each sovereign to discover whether a default might be looming.